Selling Your Veteran-Owned Business: What Happens to Your SDVOSB Status, Your Team, and Your Money

- Erik James Roberts, Founder & Chief Investment Officer | Infinitus Wealth Management

- 1 day ago

- 9 min read

When a buyer calls about your company, three questions surface almost immediately — and they're the right three. What happens to the certification we built this on? What happens to my people and our contracts? And what do I actually do with the money? Selling your veteran-owned business is one transaction with three distinct battlefields, and this article walks you through all three.

A note on who's writing this. I was in high school when the towers fell on September 11, 2001, and I knew that day that I had to serve my nation. I left for the Army immediately after graduation, determined to serve on the front lines—and I got there. I served on multiple combat deployments as an infantryman in the 101st Airborne, including during the invasion of Iraq, and later led a reconnaissance infantry team until an explosion severed my femur and left me with only a 10% chance of keeping my leg.

I kept the leg, earned the Purple Heart, and found my next mission through the Wall Street Warfighters Foundation, which introduced wounded veterans to careers in finance. From there, I spent many years in wealth management, earned a Wharton MBA, and founded Infinitus Wealth Management—an independent, fee-only fiduciary RIA certified as a Service-Disabled Veteran-Owned Small Business and registered in SAM.gov. We operate within the same federal ecosystem in which many of our veteran clients built their companies. So when I write about what a sale means for certification, contracts, and capital, I'm writing about a world I operate in.

What Happens to SDVOSB Status When Selling Your Veteran-Owned Business

The blunt version: the certification generally does not survive a sale to a non-veteran buyer. SDVOSB and VOSB status rests on majority ownership and control by the qualifying veteran — that's the entire premise of the program — so when ownership passes to a private equity firm, a strategic acquirer, or any non-veteran buyer, the eligibility that unlocked your set-aside awards typically ends with the deal. A sale to another qualifying veteran is the main path that can preserve it, and partial-sale structures that attempt to keep veteran majority control are precisely the kind of fact-specific territory where your government contracts attorney earns their fee. Nothing in this section substitutes for that analysis.

What this means practically is that your certification is priced into your deal whether anyone says so or not. Buyers separate your revenue into what they can keep without you — full-and-open awards, commercial work, contracts any owner could service — and what depended on an eligibility they will not possess. A pipeline that is heavily set-aside-dependent tends to get priced more conservatively, structured with larger earnouts, or both. The founders who do best on this dimension are the ones who saw it years early and diversified the contract base — not because set-asides are a weakness, but because revenue that survives the sale is revenue the buyer pays full price for. If you want to see the rest of the math acquirers run, I've written a companion piece on how private equity values your business.

Your Contracts and Your People

Two more realities of selling your veteran-owned business are worth knowing before the LOI. First, existing government contracts don't simply ride along with a stock certificate — transferring them to a buyer generally involves a government novation process with its own approvals and timeline, which is one reason GovCon deals close slower than commercial ones and why your counsel maps the contract portfolio early. The distinction that matters: losing SDVOSB status primarily affects future set-aside awards and recompetes; it doesn't automatically terminate work already under contract, though the details live in your specific vehicles and your attorney's analysis of them.

Second, your people are the asset. Buyers of services firms are buying cleared, credentialed, mission-experienced teams and the past performance record they generated — which is why retention packages, key-person terms, and your own transition period become negotiating chips. Founders who've led soldiers tend to negotiate this part well; you already know that taking care of the team is not sentiment, it's the value. Get the retention structure into the deal documents, not the handshake.

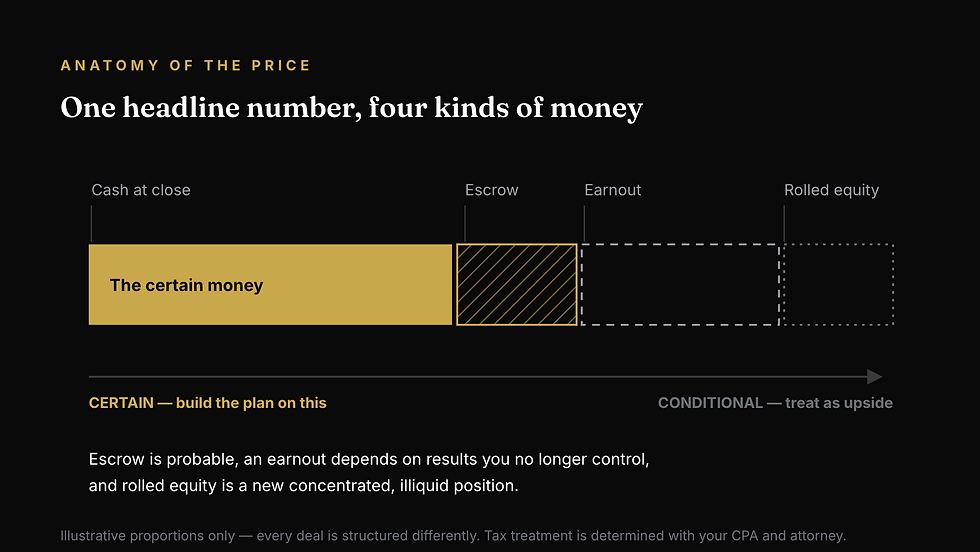

Selling Your Veteran-Owned Business: What Happens to the Money

Now the part that becomes your life after closing. The headline number in the LOI is not what lands in your account — the price arrives in pieces, on a timeline, and understanding that anatomy is the foundation of every decision that follows. Cash at close is the certain part. An escrow holdback — commonly a slice of the price held back for a year or more against representations and warranties — is probable but not guaranteed money. An earnout tied to post-close performance is conditional money, and in GovCon deals earnouts often hinge on recompete wins you no longer fully control. Rolled equity, if you take a stake in the buyer, is a new concentrated, illiquid position — often attractive, never certain. Tax treatment across all of it depends on entity type, asset-versus-stock structure, and how the price is allocated; that conversation belongs to your CPA and transaction attorney, and it should happen before the structure is locked, because after closing the options collapse to filing correctly.

Here is the planning principle for selling your veteran-owned business: build the family's plan on the certain money, and treat the conditional money as upside. A plan that requires the earnout to hit is a plan with a single point of failure — and you didn't run your company that way. The window between LOI and close, while diligence consumes everyone's attention, is exactly when the personal side should be built: how many years of family spending get secured in high-quality, short-duration assets before any dollar takes market risk; what the paced deployment schedule looks like; how the portfolio coordinates with the estate and tax work running in parallel. Done right, the day the wire lands is the day execution starts — not the day planning starts.

The First 90 Days After the Wire

The most common mistake after selling your veteran-owned business isn't a bad investment — it's speed in one direction or paralysis in the other. Proceeds that sit in a single bank account for a year lose ground quietly; proceeds deployed in a week, before the family's actual needs are mapped, take risks nobody priced. The discipline that works reads like an operations order: secure the near objective first — years of family spending in short-duration quality; then rebuild the paycheck — dividend-growth equities and directly held bonds producing income you can see on the statement, replacing the owner draw; then build the long campaign — equity strategies constructed to compound for decades, because for most founders the real mission isn't preserving the pile, it's building the family's next asset. In our practice every one of those positions is an individual stock or bond you directly own, drawn from twelve proprietary strategies and combined into one custom portfolio — the same position-level visibility you demanded from your own P&L, from a fee-only fiduciary with no commissions and nothing to sell you but judgment.

A Custom Portfolio Built Around Your Goals — Not a Model

Here is the part most founders don't expect from wealth management: after selling your veteran-owned business, there is no standard answer for what the portfolio should be — because there is no standard reason founders sell. Some of you are 45 and building the next fortune; the mission is continued aggressive growth, and the portfolio should be an engine — growth-oriented equity strategies compounding hard, sized to a founder's risk tolerance rather than a retiree's. Some of you crossed the finish line and never intend to go back; the mission is wealth protection — capital that holds its ground through every market environment, with risk management built into the construction itself: quality positions, defined limits, real diversification. Many of you want reliable income — the paycheck rebuilt from dividends and bond interest so the family's lifestyle never depends on selling anything. Some are funding a next venture and need a liquidity runway held ready without sitting idle. And nearly all of you, eventually, are building a legacy — capital constructed to outlive you and carry your name the way your company did.

After selling your veteran-owned business, we build for whichever of those is true — and usually it's a blend that shifts over the years. That is exactly what our twelve proprietary strategies exist for: they are building blocks, not products, combined into one custom portfolio of individual stocks and bonds calibrated to your specific goals, income needs, tax picture, and timeline. When the goals change — the next venture launches, the kids' funding completes, the risk appetite moves — the portfolio is recalibrated in a direct conversation with the CIO who built it, not re-slotted into the next model on a shelf. Your company was never generic. Your capital shouldn't be either.

How the Money Is Actually Managed

"Active management" is a phrase every firm uses, so here is what it means in this practice, concretely. Every position in your portfolio begins as research: individual-company fundamental analysis — the financials, the management team's execution, the durability of the competitive position — augmented by fundamental and macro-economic analysis, and distilled until only high-conviction businesses remain. Thousands of securities go into that funnel; a portfolio of individually selected stocks and bonds comes out, every one owned directly in your name and every one there for a stated reason. You ran your company on accountability at the line-item level. This is a portfolio run the same way.

Then the work continues, because markets move through cycles and a portfolio built for selling your veteran-owned business proceeds has to live through all of them. Positions are monitored continuously and adjusted when the research supports it — measured decisions, not reactive trading — with active oversight and risk management embedded in the construction itself: quality standards, diversification, defined limits. And you see all of it. Every holding on your Altruist statement, reviews with the CIO who actually makes the decisions, and reporting that shows exactly what you own, what it earned net of the fee, and why it's positioned the way it is. That is the standard of management your capital gets here — stated plainly, and answered for in person, because the person who built the portfolio is the one across the table.

Why This Firm, and Why It's Different

Infinitus Wealth Management serves veteran business owners as a deliberate practice area, and the firm's structure matches the client: veteran-built and SDVOSB certified, independent and fee-only, with portfolios of individual stocks and bonds held at Altruist, an independent custodian. There's no parent company, no product shelf, no commissions — one transparent fee, one accountable decision-maker, and a founder who has stood where you're standing on both sides: in uniform, and across the table from a balance sheet that had to fund what comes next. If selling your veteran-owned business is on your horizon — or already behind you — the conversation costs nothing and starts with your situation, not our pitch.

Frequently Asked Questions

Does SDVOSB certification transfer to the buyer of my business?

Generally, no. SDVOSB and VOSB status depends on majority ownership and control by a service-disabled veteran or veteran, so a sale to a non-veteran buyer typically ends the certification. A sale to another qualifying veteran can preserve it. Certification and eligibility questions should be confirmed with a government contracts attorney for your specific transaction.

What happens to my set-aside contracts when I sell?

Existing contracts generally require government approval to transfer to a buyer through a novation process, and the loss of SDVOSB status typically affects eligibility for future set-aside awards and recompetes rather than automatically terminating current work. The specifics depend on the contracts and the transaction — your contracts counsel drives this analysis.

How do buyers value SDVOSB-dependent revenue?

Buyers distinguish between revenue any owner could retain and revenue that depends on set-aside eligibility they will not have. Heavily set-aside-dependent pipelines are often priced more conservatively or structured with earnouts. Diversifying the contract base ahead of a sale can strengthen both the multiple and the structure.

When should I start planning what to do with the proceeds?

Before closing — ideally in the window between letter of intent and close, while diligence is running. Mapping the liquidity timeline, securing the first years of family spending, and designing the paced investment plan during that window means the capital has somewhere intelligent to go the day the wire lands.

Should I invest the sale proceeds all at once?

Deployment is generally better done on a paced, deliberate schedule than all at once, after near-term family spending has been secured in high-quality short-duration assets. The right pace depends on your circumstances, income needs, and risk tolerance.

What taxes apply when I sell my business?

Tax treatment depends on your entity type, deal structure (asset versus stock sale), and the components of the price — and the differences can be material. This is your CPA's and transaction attorney's domain, and the tax conversation should happen before the structure is locked, not after.

Veteran to Veteran

Consultation directly with Erik James Roberts, Purple Heart veteran, Wharton MBA, and the Founder & Chief Investment Officer who personally builds and manages every client portfolio. Confidential and complimentary, wherever you are in the process.

The High-Net-Worth Wealth Management Checklist for Families With $5M to $25M

Managing Portfolio Risk When Your Income and Stock Are Tied to One Company

Generating Income with Stock Options: Strategies and Insights

Navigating Tax Implications for High Net Worth Individuals: Strategies to Reduce Your Taxes

Important Disclosures

Infinitus Wealth Management is a registered investment advisory firm. This article is provided for educational and informational purposes only and does not constitute investment, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any security or to enter into any advisory relationship. Any references to specific strategies, withdrawal rates, tax provisions, or historical figures are general in nature and may not be appropriate for any individual investor.

Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Tax laws are complex, change frequently, and have unique application to individual circumstances; please consult a qualified tax professional regarding your specific situation. Social Security rules, Medicare rules, and retirement account regulations are subject to legislative and regulatory change.

The information in this article was believed to be accurate at the time of writing but is not guaranteed. Readers should consult with their own qualified advisors before making any financial decisions specific to their situation.