Retirement Wealth Management in Nashville

You spent decades building your wealth. Retirement asks a harder question: how do you turn that portfolio into reliable income that lasts — protected against bad timing, inflation, and taxes — without giving up growth? That is the work we do.

Portfolio management led by Erik James Roberts, MBA — Founder & Chief Investment Officer, Infinitus Wealth Management. Wharton MBA · U.S. Army veteran (101st Airborne) · Purple Heart recipient.

• Fiduciary • Custom Portfolios • Active Management • Investment Focused

⎯ The Shift

Retirement Changes the Entire Job of Your Portfolio

For thirty years, the goal was simple: accumulate. In retirement, the same portfolio has to do something far more delicate — produce income, survive market downturns while you're drawing from it, and still grow enough to outlast you.

Most people approaching retirement have been served by a single idea: buy, hold, and let it grow. Accumulation isn't wrong — but on its own it's incomplete the moment withdrawals begin. Growth still matters enormously in retirement; a portfolio may need to fund three decades or more of spending while inflation steadily raises the cost of that spending. What changes is that growth can no longer be pursued in isolation. It now has to coexist with the income you're drawing, the sequence in which returns arrive, and the tax treatment of every dollar that leaves the account.

This is precisely where retirement wealth management calls for active, hands-on management rather than a static model. At Infinitus, we build retirement portfolios from individual stocks and bonds and manage them directly — pursuing continued growth to help offset inflation and longevity, while shaping that growth around the income you need and the risks that matter most in this phase of life. The growth engine doesn't get switched off at retirement; it gets re-engineered to do two jobs at once.

The result is a portfolio designed for the distribution phase — one built to keep growing and keep paying, rather than an accumulation portfolio quietly hoping it holds up.

⎯ What Changes When the Paycheck Stops

The Six Risks That Define Retirement Investing

The risks that barely registered during your working years move to the center the moment you depend on your portfolio for income. This is the landscape we manage against.

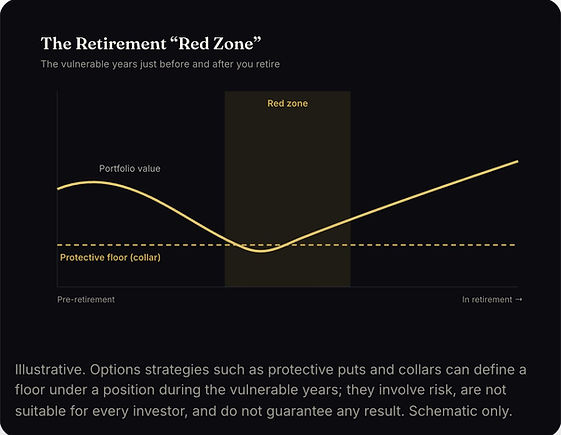

⎯ The Risk That Defines Early Retirement

Protecting Against Sequence-of-Returns Risk

It's one of the least understood — and most dangerous — risks in retirement. Two investors can earn the exact same average return over twenty years, yet one runs short of money and one doesn't, purely because of when the bad years hit.

A market decline in the first few years of retirement, while you're withdrawing income, does damage that strong later returns can't fully repair. We manage this directly through diversification, a deliberate fixed-income foundation, and, where appropriate, options-based downside protection in the vulnerable years around your retirement date.

⎯ Replacing the Paycheck

Building Reliable Income From Individual Securities

We don't hand your retirement income to a packaged product. We build it — from dividend-paying stocks, interest from bonds, and laddered fixed income — so the cash flow is transparent, controllable, and tax-aware.

-

Dividend income from high-quality individual equities

-

Bond interest and laddered maturities for predictable cash flow

-

Tax-aware municipal bonds where the after-tax math supports it

-

Principal drawn deliberately, never reactively, when needed

⎯ Capital Preservation

Defending the Years That Matter Most

The decade surrounding your retirement date carries outsized importance. A major drawdown in that window — when your balance is near its peak and withdrawals are beginning — can reshape the rest of your retirement.

Beyond diversification and a strong fixed-income base, we use disciplined options strategies where appropriate to establish downside protection during this period. The aim is straightforward: stay invested for growth while defining how much risk you're exposed to when it counts most.

⎯ Keeping More of What You've Earned

Tax-Efficient Withdrawals & Account Sequencing

In retirement, after-tax income is the number that matters. The order in which you draw from your accounts — and how the portfolio is positioned across them — can meaningfully change how long your money lasts.

⎯ Our Approach

Active, Personalized Management for the Distribution Years

No two retirements look alike, so no two portfolios should. Each is constructed around your income needs, your risk tolerance, and the legacy you intend to leave.

We build retirement portfolios from individual stocks and bonds — not mutual funds, and rarely ETFs. That direct ownership gives us control over the income your portfolio produces, the timing of every realized gain or loss, and the precise calibration of risk as your needs evolve.

Risk is actively managed: high-quality diversified equity for growth, a deliberate fixed-income foundation for stability and income, and options-based hedging where appropriate to protect against the downturns that matter most in retirement.

And you work directly with the Chief Investment Officer inside a fee-only fiduciary relationship — the person setting your strategy is the person you talk to.

What sets the retirement portfolio apart

-

Income engineered from securities you actually own

-

Sequence-of-returns risk managed deliberately

-

Downside protection in the years that matter most

-

Tax-aware withdrawals coordinated across accounts

-

Direct access to the CIO, not a call center

⎯ Local Roots, National Reach

Nashville-Based, Serving Retirees Nationwide

Based on Music Row, we work with retirees and pre-retirees across Nashville and throughout the country. Many come to us in the years just before retirement — the moment when the strategy that built their wealth needs to become a strategy that sustains it.

Whether you're a few years out or already retired and want a sharper, more active approach to your income and risk, the conversation starts the same way: directly, and on your terms.

⎯ Transparent, Fee-Only

Fees

We accept zero commissions and act as a fiduciary — mandated by law and ethically bound to put our clients’ interests first. Our fee is based on assets under management, so we do well when you do well.

No Performance Fees

We charge no performance fees. Our simple and straightforward Assets Under Management fee allows our advisors to focus on achieving our clients' goals.

No Commissions

We charge no commissions on buying and selling investments, so our interests are completely aligned as we grow and protect your accounts.

No Financial Planning Costs

A complimentary and comprehensive financial plan is available to all clients of Infinitus Wealth Management.

⎯ Working Together

How the Relationship Works

Clients come to us expecting clarity, discipline, and direct access to the person managing their capital. The process is built to deliver exactly that.

01

Discovery Call

A no-pressure conversation about your goals, holdings, and what you want your wealth to do — by phone, video, or in person.

02

Strategy Review

We review your holdings, goals, and risk profile, then share observations on how your portfolio is positioned and where a tailored approach may help.

03

Onboarding

Thoughtful, paced execution and, where appropriate, hedging — executed with intention rather than reaction.

04

Active Management

We build and manage your portfolio of individual securities, with ongoing research and protfolio reviews.

Schedule a Private Portfolio Consultation

For investors seeking disciplined portfolio management,

tactical asset allocation, and long-term capital stewardship.

Confidential discussion

No Obligation

Direct conversation with Founder & Chief Investment Officer

Learn about our Active & Personalized Portfolio Management

Explore our Investment Strategies

⎯ Frequently Asked Questions

Retirement Wealth Management — Questions Retirees Ask

How much money do I need to retire comfortably? There's no single number, because it depends on your spending, time horizon, other income sources, and how your portfolio is managed. What matters more than a headline figure is whether your portfolio can generate reliable income, withstand a poor sequence of early-retirement returns, and keep pace with inflation over a long retirement. We build portfolios around those objectives rather than a one-size-fits-all rule.

What is sequence-of-returns risk and why does it matter near retirement? It's the danger that poor returns early in retirement, combined with withdrawals, permanently reduce how long a portfolio lasts. Two retirees can earn the same average return over time yet end with very different outcomes simply because of the order in which those returns arrived. Managing this risk is central to how we structure portfolios in the years just before and after retirement.

How do you generate retirement income from a portfolio? We build income from individual securities — dividend-paying stocks, interest from bonds, and laddered fixed income — rather than relying on packaged products. This gives direct control over the holdings, the timing of cash flows, and tax-lot management. Income strategy is tailored to each client's spending needs and coordinated with tax considerations.

Can a portfolio be protected against a market crash right before retirement? Risk near retirement can be managed, though never eliminated. Alongside diversification and fixed income, we use options strategies such as protective puts and collars where appropriate to define downside on a position during the vulnerable years around retirement. These are risk-management tools used within a fiduciary framework, not guarantees of any result.

How are retirement withdrawals managed to reduce taxes? Tax-efficient withdrawal sequencing coordinates which accounts to draw from and when — balancing taxable, tax-deferred, and tax-free accounts, managing capital-gains realization, and considering opportunities such as Roth conversions. Asset location and municipal bonds can further improve after-tax results. Tennessee residents also benefit from no state income tax following the Hall tax repeal in 2021.

Should I use individual stocks and bonds or funds in retirement? Infinitus builds custom portfolios from individual stocks and bonds rather than mutual funds, and rarely uses ETFs. Owning individual securities provides direct control over income timing, tax-lot management, and risk calibration — which is especially valuable when a portfolio is funding ongoing withdrawals rather than simply accumulating.

What does Infinitus Wealth Management charge? Infinitus is a fee-only fiduciary and charges asset-based advisory fees beginning at 1.00% on portfolios under $1 million and scaling down toward 0.80% at $10 million and above. There are no commissions and no performance fees.

⎯ Explore Further

Related Strategies & Reading

Disclosure: Infinitus Wealth Management is a registered investment adviser. Registration does not imply a certain level of skill or training. All investments involve risk, including the potential loss of principal. No investment strategy can guarantee returns or eliminate risk, and past performance is not indicative of future results. Advisory services are offered only pursuant to a written advisory agreement.