Investment Strategies · Infinitus Wealth Management

Tax-Exempt Municipal Bond Strategy

Investment management in Nashville

The Tax-Exempt Municipal Bond Strategy is designed for investors seeking tax-exempt income while emphasizing capital preservation and portfolio stability. Interest is generally exempt from federal income tax — and, for bonds issued in your own state, often from state and local tax as well. We invest in high-quality municipal bonds issued by state and local governments and related public entities, prioritizing credit quality, disciplined risk assessment, and structured portfolio construction.

Strategy designed and managed by Erik James Roberts, MBA — Founder & Chief Investment Officer, Infinitus Wealth Management. Wharton MBA · Fee-only fiduciary.

⎯ Strategy Philosophy

Why Tax-Exempt Municipal Bonds Belong in a High-Bracket Portfolio

For investors in higher tax brackets, the return that matters is the return you keep. Municipal bonds can play an important role in a diversified portfolio precisely because their interest is generally exempt from federal income tax — and that exemption can meaningfully enhance after-tax returns while supporting a more stable investment experience than many other income-producing assets.

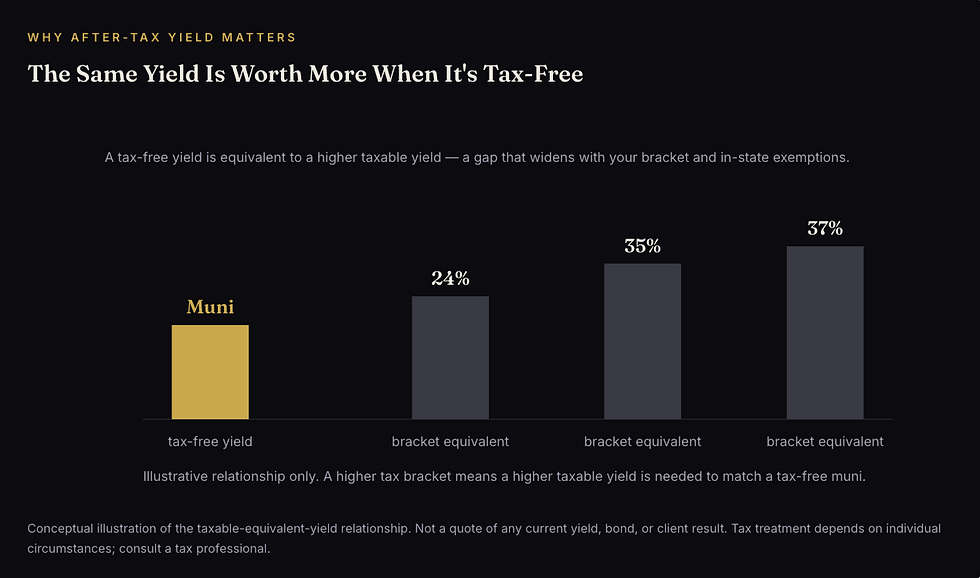

The advantage is easy to underappreciate until it is measured. A tax-free municipal yield is worth far more to a high-bracket investor than the same nominal yield on a taxable bond, because no share of it is surrendered to the IRS each year. Comparing bonds on their stated yield alone, without adjusting for taxes, quietly understates what a quality muni actually delivers to the investor who holds it.

The exemption can reach further than federal tax alone. When an investor holds bonds issued within their own state of residence, the interest is often exempt from state and local income tax as well — making those bonds effectively triple tax-free for residents of high-tax states like California and New York. This is where a separately managed account earns its keep: rather than owning a national bond fund indifferent to where you live, your portfolio can be built around your state to pursue in-state tax advantages wherever they apply.

Our approach emphasizes credit quality, the financial strength of issuers, and disciplined bond selection to support reliable income generation and long-term capital preservation. Tax-exempt municipal bond investing, done well, is not about reaching for the highest headline yield — it is about assembling a portfolio of financially sound issuers whose after-tax income can compound quietly and dependably for years.

⎯ Investment Focus

What We Look for in a High-Quality Municipal Bond

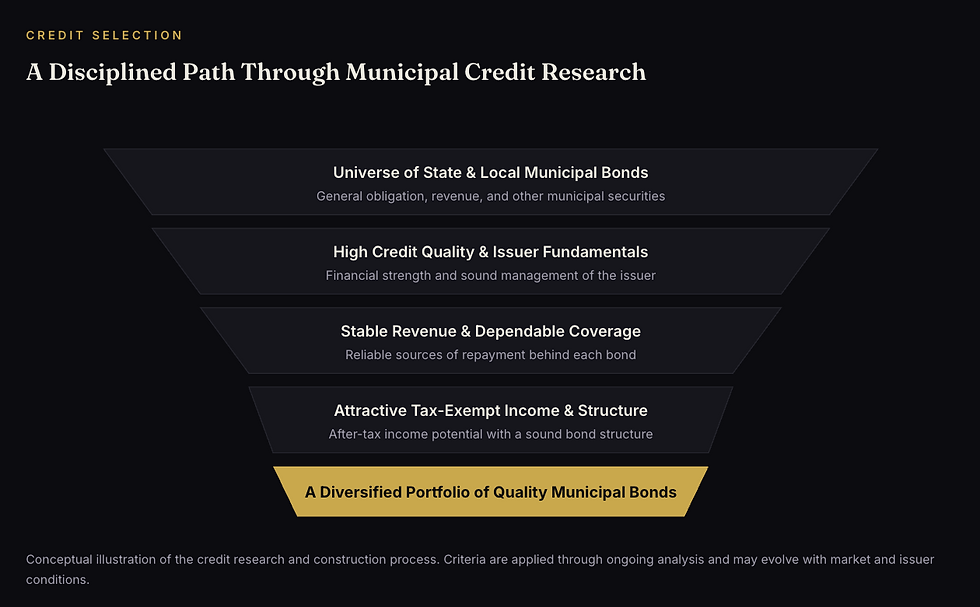

Every position begins with credit research on the specific issuer. We are not buying a bond index or a fund wrapper — we are evaluating individual municipal bonds, one issuer at a time, against a demanding standard. The portfolio emphasizes bonds that demonstrate high credit quality and strong issuer fundamentals, stable sources of revenue and sound financial management, attractive tax-exempt income potential, diversification across sectors, issuers, and regions, and structures designed to support consistent income and risk management.

The distinction between the two main municipal bond types matters here. General obligation bonds are backed by the full taxing power of the issuing government, while revenue bonds are repaid from the income of a specific project such as a water system, toll road, or public utility. Each carries a different credit profile, and the strategy may include general obligation bonds, revenue bonds, and other municipal securities aligned with the strategy's quality and income objectives — chosen on their individual merits rather than by a formula.

What unites the portfolio is not a single sector or state — it is a standard. Whether a bond is a general obligation issue from a fiscally strong municipality or a revenue bond backed by an essential public service, it must clear the same bar: sound issuer finances, dependable revenue, and a structure that serves the portfolio's income and preservation goals.

⎯ Portfolio Approach

How the Municipal Bond Portfolio Is Constructed

The strategy is built through disciplined credit analysis and ongoing monitoring of issuer financial health, economic conditions, and market dynamics. A bond earning a place in the portfolio at purchase is not the end of the work — issuer finances are watched over the life of every holding, because a municipal bond's safety rests on the continued health of the entity standing behind it.

Beyond individual credit selection, portfolio-level decisions shape the strategy's stability. Duration and interest rate sensitivity are managed deliberately, since bond prices move inversely to interest rates and a portfolio's duration determines how sharply. Sector exposure is balanced so the portfolio does not depend on the fortunes of any single type of issuer or region. The goal is to provide consistent tax-efficient income while managing interest rate and credit risk together, rather than optimizing one at the expense of the other.

Because every portfolio is separately managed in your own account, construction also reflects your individual circumstances — your state of residence and its tax treatment, your existing holdings, and your income needs — rather than forcing your capital into a one-size-fits-all bond fund.

⎯ Risk Perspective

Managing Interest Rate and Credit Risk in Municipal Bonds

Municipal bonds are subject to risks including interest rate changes, credit risk, and market fluctuations. The strategy manages these through a focus on higher-quality issuers, diversification across sectors and regions, and active oversight of every holding. Two risks deserve particular attention, because they behave differently and are managed differently.

Interest rate risk is the tendency of bond prices to fall when rates rise and rise when rates fall. The strategy addresses it through deliberate duration management and, where appropriate, a laddered structure that returns principal at staggered intervals — creating natural reinvestment points rather than locking the entire portfolio into a single point on the yield curve. Credit risk is the possibility that an issuer cannot meet its obligations; the strategy addresses it by emphasizing financially strong issuers and monitoring their health continuously, not just at purchase.

Capital preservation is a priority, and municipal bonds have historically been a relatively stable asset class. Bond prices can still fluctuate based on market conditions, and no strategy can eliminate risk. What disciplined credit work and thoughtful structure provide is a steadier foundation for dependable, tax-advantaged income across changing markets.

⎯ The Infinitus Difference

Municipal Bond Investing with Individual Bonds, Not Funds

Most investors who want municipal bond exposure are handed a muni bond fund or ETF — a wrapper holding hundreds or thousands of bonds nobody at the firm has individually researched, with a perpetual average maturity that never actually matures, embedded fees, and no transparency into what is owned. We take the opposite approach. Municipal bond investing at Infinitus means a portfolio of individually selected bonds, each one credit-researched, understood, and owned for a specific reason, held directly in your own account.

That structure has advantages a fund cannot match. Because you own individual bonds with defined maturities, you know exactly when each returns its principal — a bond fund's share price simply floats with the market, with no maturity date to anchor it. Because the portfolio is separately managed, it can be built around your state of residence to pursue state-tax advantages where they apply, and around your specific income timeline. And because our Founder & Chief Investment Officer makes every credit decision directly, the person managing your capital is the same person you speak with.

As a fee-only independent fiduciary, we are compensated only by the transparent advisory fee our clients pay us. No commissions, no bond markups, no products — no incentive to put anything in your portfolio except what we believe belongs there.

⎯ Objective

The Goal of the Strategy

To provide federally tax-exempt income and portfolio stability by investing in a diversified portfolio of high-quality municipal bonds — supporting dependable after-tax income and long-term capital preservation.

Ultimately, the strategy is built for capital that needs to generate reliable, tax-advantaged income while staying intact — a fit for high-bracket professionals and executives, retirees drawing steady income, and anyone who values keeping more of what their portfolio earns.

Within a broader portfolio, the Tax-Exempt Municipal Bond Strategy often serves as the tax-efficient income anchor. Clients frequently pair it with our U.S. & Global Bonds strategy for broader fixed-income exposure, with Dividend Income Growth for equity income, or with our Stable Value Equity and growth strategies to balance income, stability, and appreciation in the proportions that fit their goals.

⎯ Working Together

How the Relationship Works

Clients come to us expecting clarity, discipline, and direct access to the person managing their capital. The process is built to deliver exactly that.

01

Discovery Call

A no-pressure conversation about your goals, holdings, and what you want your wealth to do — by phone, video, or in person.

02

Strategy Review

We review your holdings, goals, and risk profile, then share observations on how your portfolio is positioned and where a tailored approach may help.

03

Onboarding

Thoughtful, paced execution and, where appropriate, hedging — executed with intention rather than reaction.

04

Active Management

We build and manage your portfolio of individual securities, with ongoing research and protfolio reviews.

Schedule a Private Portfolio Consultation

For investors seeking disciplined portfolio management,

tactical asset allocation, and long-term capital stewardship.

Confidential discussion

No Obligation

Direct conversation with Founder & Chief Investment Officer

Learn about our Active & Personalized Portfolio Management

Explore our Investment Strategies

⎯ Common Questions

Tax-Exempt Municipal Bond Strategy FAQ

What is the Tax-Exempt Municipal Bond Strategy? It is a fixed-income strategy from Infinitus Wealth Management in Nashville designed for investors seeking federally tax-exempt income while emphasizing capital preservation and portfolio stability. The portfolio holds individual municipal bonds issued by state and local governments and related public entities, selected through our own credit research and held directly in your account rather than inside a bond fund.

Why are municipal bonds considered tax-efficient? Interest from municipal bonds is generally exempt from federal income tax. When you hold bonds issued within your own state of residence, the interest is often exempt from state and local income tax as well — making those bonds effectively triple tax-free for residents of high-tax states such as California or New York. For investors in higher brackets, this can meaningfully increase after-tax income: a tax-free municipal yield is equivalent to a higher taxable yield, and the gap grows with both your bracket and any in-state exemption. Because states differ (some, like Tennessee, impose no income tax at all, so there is no additional state benefit), the advantage is specific to your situation — and we coordinate with your tax professional to capture it.

What is the difference between general obligation and revenue bonds? General obligation bonds are backed by the full taxing power of the issuing government. Revenue bonds are repaid from the income of a specific project, such as a water system, toll road, or public utility. Each carries a different credit profile, and the strategy may include both — along with other municipal securities — chosen on their individual credit merits rather than by a fixed formula.

How does the strategy manage interest rate and credit risk? Interest rate risk is managed through deliberate duration decisions and, where appropriate, a laddered structure that returns principal at staggered intervals to create natural reinvestment points. Credit risk is managed by emphasizing financially strong issuers, diversifying across sectors and regions, and monitoring issuer health continuously over the life of each bond — not only at purchase. These techniques manage risk; they cannot eliminate it, and bond prices can still fluctuate.

Who is this strategy designed for? Investors seeking dependable, tax-advantaged income with an emphasis on capital preservation — particularly high-bracket professionals and executives, retirees drawing steady income, and families who want to keep more of what their fixed income earns. Suitability and the tax benefit itself depend on your individual bracket, state of residence, and goals, and are always assessed individually.

Can I combine this strategy with other Infinitus strategies? Yes. Most clients don't hold a single strategy in isolation — we frequently combine multiple Infinitus strategies into one cohesive portfolio built around your goals, risk tolerance, and time horizon. This strategy can be paired with more growth-oriented, income-focused, or conservative approaches to balance appreciation, stability, and cash flow in the proportions that fit you. The right blend depends entirely on your circumstances; we determine it together during the strategy review and adjust it over time as your needs change. Because we build everything from individual securities in an account you own, combining strategies is seamless and fully transparent.

What are your advisory fees? Fees are a single transparent percentage of assets under management on a four-tier schedule: 1.00% under $1M, 0.95% from $1M to $4.99M, 0.90% from $5M to $9.99M, and 0.80% at $10M and above. A complimentary financial plan is included.

Who does Infinitus Wealth Management work with? Infinitus serves a diverse range of clients across Nashville and beyond, including high-net-worth individuals and families, business owners and founders, corporate professionals and executives, retired and pre-retirement investors, professional athletes, musicians and entertainers, endowments, foundations and nonprofits, and young professionals building long-term wealth.

How do I get started with Infinitus? Getting started is simple. Schedule a complimentary, no-obligation private portfolio consultation directly with Erik James Roberts, Founder and Chief Investment Officer. We’ll discuss your goals, current portfolio, timeline, and risk tolerance to determine how Infinitus can help you grow and protect your wealth. Contact us at erik.roberts@infinituswealth.com or request your consultation today.

⎯ Explore Further

Investment Strategies Built Around Your Goals

Disclosure: Infinitus Wealth Management is a registered investment adviser. Registration does not imply a certain level of skill or training. All investments involve risk, including the potential loss of principal. No investment strategy can guarantee returns or eliminate risk, and past performance is not indicative of future results. Advisory services are offered only pursuant to a written advisory agreement.