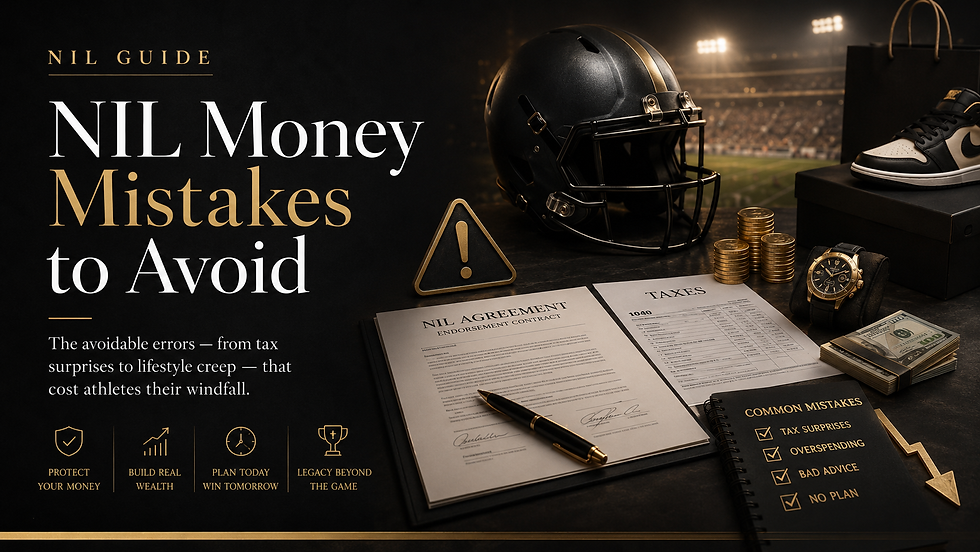

NIL Money Mistakes to Avoid: The 7 Errors That Cost Athletes Their Windfall — and the Fix for Each One

- Erik James Roberts, Founder & Chief Investment Officer | Infinitus Wealth Management

- 1 day ago

- 8 min read

Here's the encouraging truth about NIL money mistakes: nearly all of them are system failures, not character failures — and systems can be fixed in an afternoon. The athletes who stumble with NIL money aren't careless or foolish. They're 19-year-olds handed business-owner responsibilities with no operating manual, in an environment where the money is visible to everyone around them. Give the same athlete a simple system, and the mistakes below become nearly impossible to make.

That's how this guide is built. Each of the seven NIL money mistakes comes paired with its specific fix — usually a single habit or account structure — so you can treat this less like a warning label and more like a pre-flight checklist. Run through it once, install the fixes, and your NIL money starts working the way it should: funding your life today and compounding for the fifty years after your eligibility ends.

The Tax-Side NIL Money Mistakes: Where Most Trouble Starts

Mistake #1: Spending the gross, not the net

The deal announcement says $50,000, and it feels like $50,000 — but NIL income is self-employment income, which means nothing is withheld and a meaningful slice of every payment already belongs to taxes. Self-employment tax runs 15.3% on net earnings, federal income tax stacks on top, and depending on where deals happen, state tax can too. An athlete who builds a spending plan on the announced number is planning with money that was never fully theirs.

Athletes who plan on the gold number never experience a "tax surprise" — because the reserve was funded before the money ever felt spendable.

The fix — The day any NIL payment arrives, move 25–30% into a separate tax account. Automate it if your bank allows. Everything left is genuinely yours to plan with.

Mistake #2: Missing quarterly estimated payments

Because nothing is withheld from NIL income, the IRS generally expects payment four times a year — typically April 15, June 15, September 15, and January 15. Athletes who wait until filing season can face underpayment penalties even when they ultimately pay in full. The good news: if Mistake #1 is fixed, this one nearly fixes itself — the money is already sitting in the tax account, and each deadline becomes a five-minute transfer. The full mechanics are in our guide, NIL Taxes Explained for College Athletes.

The fix — Put the four deadlines in your phone with reminders one week out, and confirm the set-aside percentage annually with a CPA once income grows.

Mistake #3: No bookkeeping — and forgetting that free stuff counts

Mixing NIL payments with everyday spending money in one checking account makes three things nearly impossible: knowing what you earned, proving your deductible expenses, and catching the income that never came with a form. Remember that a 1099 is a reporting document, not a taxability trigger — payments through apps count, payments under reporting thresholds count, and product-for-post deals are generally taxable at fair market value. $3,000 of free gear in exchange for content is usually $3,000 of income.

The fix — One dedicated NIL bank account, every deal's paperwork in one folder, and a monthly "money hour" to log income and file receipts. An hour a month keeps deductions captured and April boring.

The Lifestyle-Side NIL Money Mistakes: Quiet, Comfortable, Expensive

Mistake #4: Lifestyle creep — converting a windfall into fixed costs

This is the subtlest mistake on the list because every individual step feels reasonable. A bigger deal lands, so the apartment upgrades. Another lands, so the car payment does. None of it is reckless in isolation — the trap is that income can be temporary while fixed costs are contractual. NIL income can end with eligibility; the lease and the loan don't. Athletes who upgrade their fixed costs with every deal are converting a windfall into obligations, and they often can't say when it happened because no single decision felt like the moment.

Gray is lifestyle; gold is invested growth. Same deals, same income — the only difference is where each raise was routed.

The fix — Set a fixed monthly lifestyle number you're genuinely happy with, and route income growth by percentage into investments instead of into fixed costs. Upgrade the lifestyle deliberately, on an annual review — not deal by deal. Splurge from the flexible bucket, in cash, on things that don't create monthly obligations.

Mistake #5: Becoming the family bank without a plan

Wanting to take care of the people who got you here is one of the best instincts an athlete can have — and it deserves a structure, not improvisation. Ad-hoc giving creates two problems: the amounts compound invisibly, and every individual request becomes an emotional negotiation. The generous move and the smart move are the same move: decide the annual giving number in advance, calmly, as part of the plan.

The fix — Set a defined annual family-and-giving amount you can sustain, share the framework with your inner circle once, and let "it's already allocated for this year" do the hard conversations for you. Generosity by design beats generosity by pressure — for everyone involved.

The Investing-Side NIL Money Mistakes: The Visible One and the Invisible One

Mistake #6: The unvettable pitch

Visible money attracts pitches — the friend's startup, the cousin's real estate flip, the trending token, the teammate's "guaranteed" opportunity. Most aren't scams; they're simply investments that can't be valued, can't be sold, and can't be verified — which makes them wrong for a young portfolio regardless of intent. The professional's move isn't cynicism. It's a filter that runs the same way every time: Do I understand exactly how this makes money? Can I value it and sell it if I choose? Has a fiduciary with no commission on the outcome reviewed it?

The fix — Route every pitch through the three questions, and make "send it to my advisor" your standard reply. It protects the money and the friendship — the "no" comes from your process, not from you.

Mistake #7: Letting the money sit — the invisible mistake

Nothing dramatic happens with this one. No bad deal, no tax notice — just NIL money accumulating in a checking account for a year, then two, while the most valuable asset an athlete owns quietly drains: compounding runway. Dollars invested at 19 have more time to grow than any dollars you'll ever earn again, and every year of "I'll figure out investing later" spends that advantage on nothing.

The fix isn't investing more — it's investing the same amount sooner. Time, not timing, does the work.

The fix — After taxes and a cash reserve, put NIL money to work on a schedule: a Roth IRA first (NIL is earned income, which unlocks it), then a taxable investment portfolio. The full playbook is in our companion guide, How College Athletes Can Build Wealth From NIL.

The Pattern Behind All Seven: Decisions vs. Systems

Look back across the list and one pattern emerges: every mistake happens when money requires a fresh decision, and every fix replaces that decision with a system. The tax surprise disappears when the set-aside is automatic. Lifestyle creep disappears when the baseline is fixed and raises are routed. The bad pitch disappears when the filter runs the same way every time. The idle cash disappears when investing happens on a schedule instead of a mood.

That's the real lesson of NIL money mistakes: they're not tests of willpower, and avoiding them doesn't require becoming a different person. It requires one afternoon of design — accounts opened, percentages chosen, automations set — and one hour a month of maintenance. Design once, and the system makes the right call on every payment for the rest of your career, including the professional contract that may follow.

Frequently Asked Questions

What is the most common NIL money mistake?

Spending the gross instead of the net — building a lifestyle around the announced figure before taxes are set aside. NIL income is self-employment income with nothing withheld, so roughly 25–30% of most payments belongs to taxes. The fix: move the tax slice to a separate account the day every payment arrives.

What is lifestyle creep and why does it hurt NIL athletes?

Lifestyle creep is rising income quietly converting into rising fixed costs — apartment, car payment, subscriptions — that persist after the income that justified them. For athletes whose income can end with eligibility, the fix is a fixed lifestyle baseline with income growth routed to investments by percentage.

Do college athletes owe taxes on NIL income even without a 1099?

Yes. All NIL income is taxable whether or not a form arrives — including free products and services received in exchange for promotion, which are generally taxable at fair market value. A dedicated NIL bank account and monthly bookkeeping keep it all tracked.

How should NIL athletes handle investment pitches from friends and family?

Three questions: Do I understand exactly how it makes money? Can I value it and sell it if I choose? Has a fiduciary with no commission on the outcome reviewed it? Anything that fails gets a polite pass — and "send it to my advisor" protects both the money and the relationship.

Is leaving NIL money in a checking account a mistake?

It's the least visible one — nothing dramatic happens, but every year of delay spends compounding runway that can't be bought back. After taxes and a cash reserve, NIL money belongs in an investment plan: Roth IRA first, then a taxable portfolio.

How does Infinitus Wealth Management help NIL athletes avoid these mistakes?

Infinitus is an independent, fee-only fiduciary RIA in Nashville serving athletes, musicians, and entertainers. Every NIL relationship includes a complimentary financial plan, coordination with your CPA and family, systems for taxes and cash flow, and a custom portfolio of individual stocks and bonds built to scale into a professional career.

Talk to Infinitus About Building Your Custom Portfolio

At Infinitus Wealth Management, we build every client a custom portfolio from individual stocks and individual bonds—never mutual funds, rarely an ETF—actively managed and hedged with options where it strengthens the portfolio. We are an independent, fee-only fiduciary: no commissions, no proprietary products, no conflicts pulling against you. Our twelve proprietary strategies give us the range to tailor a portfolio to your tax situation, income needs, and goals, whether you are early in building serious wealth or managing well into eight figures.

If you would like a clear-eyed look at how your current portfolio is actually structured—what it is costing you in fees and tax drag, whether it is being managed at the level of individual holdings, and whether your advisor’s incentives are genuinely aligned with yours—we welcome the conversation. Our complimentary portfolio analysis gives you an objective, holding-level assessment and a direct view of what a custom Infinitus portfolio would look like for you.

The High-Net-Worth Wealth Management Checklist for Families With $5M to $25M

Managing Portfolio Risk When Your Income and Stock Are Tied to One Company

Generating Income with Stock Options: Strategies and Insights

Navigating Tax Implications for High Net Worth Individuals: Strategies to Reduce Your Taxes

Important Disclosures

Infinitus Wealth Management is a registered investment advisory firm. This article is provided for educational and informational purposes only and does not constitute investment, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any security or to enter into any advisory relationship. Any references to specific strategies, withdrawal rates, tax provisions, or historical figures are general in nature and may not be appropriate for any individual investor.

Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Tax laws are complex, change frequently, and have unique application to individual circumstances; please consult a qualified tax professional regarding your specific situation. Social Security rules, Medicare rules, and retirement account regulations are subject to legislative and regulatory change.

The information in this article was believed to be accurate at the time of writing but is not guaranteed. Readers should consult with their own qualified advisors before making any financial decisions specific to their situation.