NIL Taxes Explained for College Athletes: 1099 Income, Self-Employment Tax, and Quarterly Estimates

- Erik James Roberts, Founder & Chief Investment Officer | Infinitus Wealth Management

- 2 days ago

- 8 min read

Your first NIL deal does something bigger than put money in your account — it makes you a business owner in the eyes of the IRS. That's a genuine achievement, and it comes with a new set of rules. NIL taxes work nothing like the paycheck from a summer job: there's no employer withholding anything for you, self-employment tax applies on top of regular income tax, and the IRS expects payments four times a year — not just in April. This guide explains exactly how it works, so you can run your NIL income like the business it is.

Here's the mindset shift that matters most: none of this is a burden — it's the operating manual for a real enterprise you now own. The athletes who master these basics in their first NIL year carry that skill set straight into professional contracts, endorsement income, and every business venture that follows. Learning to manage NIL taxes at 19 is a head start most entrepreneurs would kill for.

NIL Taxes 101: You're Not an Employee — You're a Business

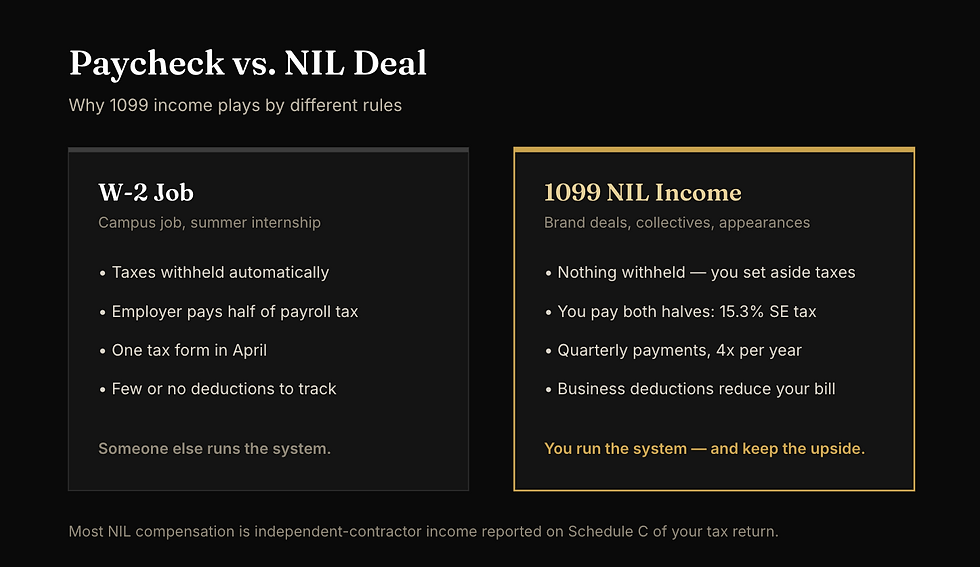

When a brand, collective, or local business pays you for your name, image, and likeness, you're almost never their employee. You're an independent contractor — a one-person business providing marketing services. That single distinction drives everything else about how NIL income is taxed.

The trade is real: 1099 income asks more of you administratively — and gives you deductions, planning flexibility, and business experience in return.

Three ground rules before anything else:

All NIL income is taxable — with or without a form. A 1099 is a reporting document, not a trigger. If a collective pays you $1,500 and no form ever arrives, that $1,500 is still taxable income you're responsible for reporting. (Note for 2026: the federal 1099 reporting threshold for businesses rose from $600 to $2,000 in payments — which means fewer forms will arrive, not less tax owed. Your own records matter more than ever.)

Free stuff counts. Product-for-post deals — apparel, gear, vehicle use, travel — are generally taxable at fair market value. $3,000 of free product in exchange for promotion is usually $3,000 of income.

The threshold is low. Self-employment tax kicks in once net self-employment earnings hit just $400 for the year. Almost every NIL athlete crosses it.

Self-Employment Tax: The Part of NIL Taxes Nobody Warns You About

At a W-2 job, Social Security and Medicare taxes are split with your employer — you pay 7.65%, they pay 7.65%. As an NIL athlete, you're both the employee and the employer, so you pay both halves: 15.3% self-employment tax on your net NIL earnings, on top of regular federal income tax.

Two pieces of good news soften the math. First, SE tax is calculated on 92.35% of your net earnings, not the full amount. Second, half of the SE tax you pay is deductible when figuring your income tax. And because NIL income is business income, qualified business expenses reduce the taxable amount before any of these taxes apply.

Notice what did the heavy lifting: legitimate business expenses reduced profit before a single tax was calculated. Tracking expenses isn't paperwork — it's a raise you give yourself.

Deductions: the reward for running it like a business

Ordinary and necessary business expenses reduce your NIL profit dollar for dollar before taxes apply. For most NIL athletes, that can include agent or marketing-rep fees, content-creation equipment (camera, lighting, editing software), travel to appearances and signings, a reasonable business-use portion of your phone, website and branding costs, and training expenses tied directly to paid content. Keep receipts, use a separate bank account for NIL money, and log expenses monthly — clean books are what turn deductions from a theory into savings.

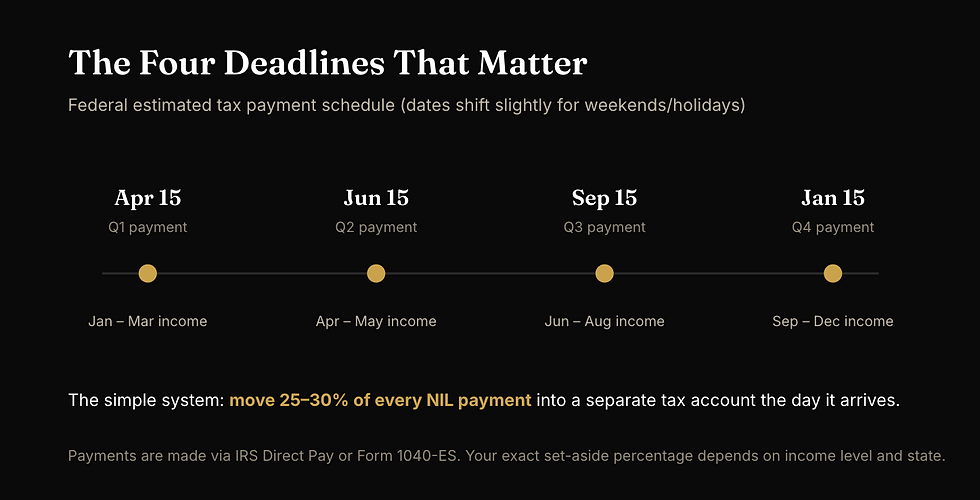

Quarterly Estimates: The NIL Taxes Calendar That Keeps You Ahead

Because nothing is withheld from NIL payments, the IRS generally expects you to pay as you earn — four estimated payments across the year. Athletes who expect to owe $1,000 or more in tax for the year typically need to make them. Miss the deadlines and you can face underpayment penalties even if you pay everything at filing time. Hit them, and April becomes a non-event.

Athletes who automate the set-aside never feel quarterly payments at all — the money was never "theirs" to spend in the first place, and every deadline is just a transfer.

The set-aside rule that removes all the stress

The entire quarterly system runs on one habit: the day an NIL payment lands, move 25–30% into a separate tax account. For most college athletes — whose total income keeps them in lower federal brackets — that range covers self-employment tax plus income tax with room to spare, and anything left over after filing becomes a bonus. Athletes with six-figure NIL income should set the percentage with a CPA, because higher brackets and safe-harbor rules change the math.

State Taxes, Scholarships, and the Details Worth Knowing

Where you earn matters — and Tennessee athletes have an edge

Tennessee has no state income tax on wages or self-employment income, which means athletes at Tennessee schools keep more of every NIL dollar than peers in most other states. But NIL income can be taxable where the work happens: an appearance, camp, or shoot in another state may create a filing obligation there. Athletes who transfer schools mid-year, or whose parents claim them as dependents in another state, should get the residency picture confirmed by a CPA early.

You can still be your parents' dependent — and you still file your own return

Earning NIL income doesn't automatically end your dependent status, but it does mean you'll generally file your own tax return reporting the business income. It's also a family conversation worth having early: NIL income is your earned income, reported under your Social Security number, and it can affect need-based financial aid calculations. A ten-minute conversation between your parents and a CPA in year one prevents surprises in year two.

Payments through apps still count

Venmo, PayPal, Cash App — the payment method changes nothing. Income is income however it arrives, and keeping NIL payments in a dedicated account (rather than mixed with pizza money) is the single easiest bookkeeping upgrade an athlete can make.

From NIL Taxes to NIL Wealth: The Bigger Opportunity

Taxes are only half the story — and honestly, the smaller half. The athletes who treat NIL income as seed capital rather than spending money are giving themselves the most powerful gift in finance: decades of compounding. Dollars invested at 19 or 20 have more time to grow than dollars invested at any other point in your life, and even modest amounts put to work during college can grow into a meaningful foundation by the time your playing days end.

That's how we approach NIL relationships at Infinitus: the tax system is the floor, not the ceiling. We coordinate with your CPA on the quarterly mechanics, then build the part most NIL guides never mention — an actual investment plan, constructed from individual stocks and bonds and tailored to your timeline, so your name, image, and likeness fund something that outlasts them all. And because we work with professional athletes and entertainers every day from our Nashville office, the plan you start in college is built to scale into a draft-day contract, a record deal, or the business you launch after sport.

Frequently Asked Questions

Do college athletes have to pay taxes on NIL income?

Yes. NIL income is taxable, and in most cases it's self-employment income — subject to both federal income tax and the 15.3% self-employment tax once net earnings reach just $400 for the year. That's true whether you're paid in cash, through an app, or in free products.

Is NIL income taxed even without a 1099?

Yes. A 1099 is a reporting form, not a trigger for taxation. All NIL income is taxable whether or not a form arrives, and the athlete is responsible for tracking and reporting it — which is why your own records matter more than any paperwork a brand sends.

What is self-employment tax on NIL income?

It's the 15.3% tax covering Social Security and Medicare for people who work for themselves — both the employee and employer halves of payroll tax. It applies to net NIL earnings above $400 per year, in addition to regular income tax. Half of it is deductible when calculating your income tax.

When are quarterly estimated taxes due for NIL athletes?

Generally April 15, June 15, and September 15, with the final payment the following January 15 (dates shift slightly for weekends and holidays). Missing them can trigger underpayment penalties even if you pay in full when you file.

Are free products and gifts from NIL deals taxable?

Generally yes. Non-cash compensation — apparel, gear, vehicle use, travel, or meals provided in exchange for promotion — is typically taxable at its fair market value, even though no money changed hands.

How does Infinitus Wealth Management help NIL athletes?

Infinitus is an independent, fee-only fiduciary RIA in Nashville working with athletes, musicians, and entertainers. For NIL athletes, that means building the financial system around the income — tax set-asides, CPA coordination, and an investment plan of individual stocks and bonds that puts early earnings to work — with a complimentary financial plan included in every relationship.

Talk to Infinitus About Building Your Custom Portfolio

At Infinitus Wealth Management, we build every client a custom portfolio from individual stocks and individual bonds—never mutual funds, rarely an ETF—actively managed and hedged with options where it strengthens the portfolio. We are an independent, fee-only fiduciary: no commissions, no proprietary products, no conflicts pulling against you. Our twelve proprietary strategies give us the range to tailor a portfolio to your tax situation, income needs, and goals, whether you are early in building serious wealth or managing well into eight figures.

If you would like a clear-eyed look at how your current portfolio is actually structured—what it is costing you in fees and tax drag, whether it is being managed at the level of individual holdings, and whether your advisor’s incentives are genuinely aligned with yours—we welcome the conversation. Our complimentary portfolio analysis gives you an objective, holding-level assessment and a direct view of what a custom Infinitus portfolio would look like for you.

The High-Net-Worth Wealth Management Checklist for Families With $5M to $25M

Managing Portfolio Risk When Your Income and Stock Are Tied to One Company

Generating Income with Stock Options: Strategies and Insights

Navigating Tax Implications for High Net Worth Individuals: Strategies to Reduce Your Taxes

Important Disclosures

Infinitus Wealth Management is a registered investment advisory firm. This article is provided for educational and informational purposes only and does not constitute investment, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any security or to enter into any advisory relationship. Any references to specific strategies, withdrawal rates, tax provisions, or historical figures are general in nature and may not be appropriate for any individual investor.

Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Tax laws are complex, change frequently, and have unique application to individual circumstances; please consult a qualified tax professional regarding your specific situation. Social Security rules, Medicare rules, and retirement account regulations are subject to legislative and regulatory change.

The information in this article was believed to be accurate at the time of writing but is not guaranteed. Readers should consult with their own qualified advisors before making any financial decisions specific to their situation.