Best Financial Advisor for Retirees in Nashville

- Erik James Roberts, Founder & Chief Investment Officer | Infinitus Wealth Management

- Apr 27

- 6 min read

Updated: Jul 29

Retirement is often portrayed as a finish line. In practice, it is something more demanding: the beginning of a new financial phase in which wealth must work harder, last longer, and be managed with greater precision than ever before.

During working years, mistakes can often be corrected with time, continued earnings, and new contributions. In retirement, the margin for error narrows. Markets still fluctuate. Inflation still erodes purchasing power. Taxes still matter. Yet portfolios may now be expected to fund lifestyle, family priorities, charitable goals, travel, healthcare costs, and multigenerational legacy ambitions.

For retirees in Nashville, selecting the right financial advisor is therefore not a casual decision. It is a capital stewardship decision.

The best financial advisor for retirees is rarely defined by the loudest advertising or the broadest promises. More often, it is the advisor who combines judgment, discipline, sophisticated portfolio management, personal accountability, and the ability to guide clients calmly through changing markets.

As Nashville continues to attract successful professionals, entrepreneurs, executives, physicians, and affluent families, retirees increasingly seek something beyond generic financial planning. They want thoughtful investment management, tax awareness, and confidence that their life’s work is being handled with seriousness.

Retirement Requires a Different Kind of Advice

Many investors enter retirement with portfolios built for accumulation rather than distribution.

That distinction matters.

A portfolio designed to grow during peak earning years may not be optimized for the realities of retirement, where priorities often include:

Reliable income without unnecessary stress

Protection from large market drawdowns

Growth to outpace inflation over decades

Tax-efficient withdrawals

Estate and legacy considerations

Simplicity and organization

Confidence during uncertain markets

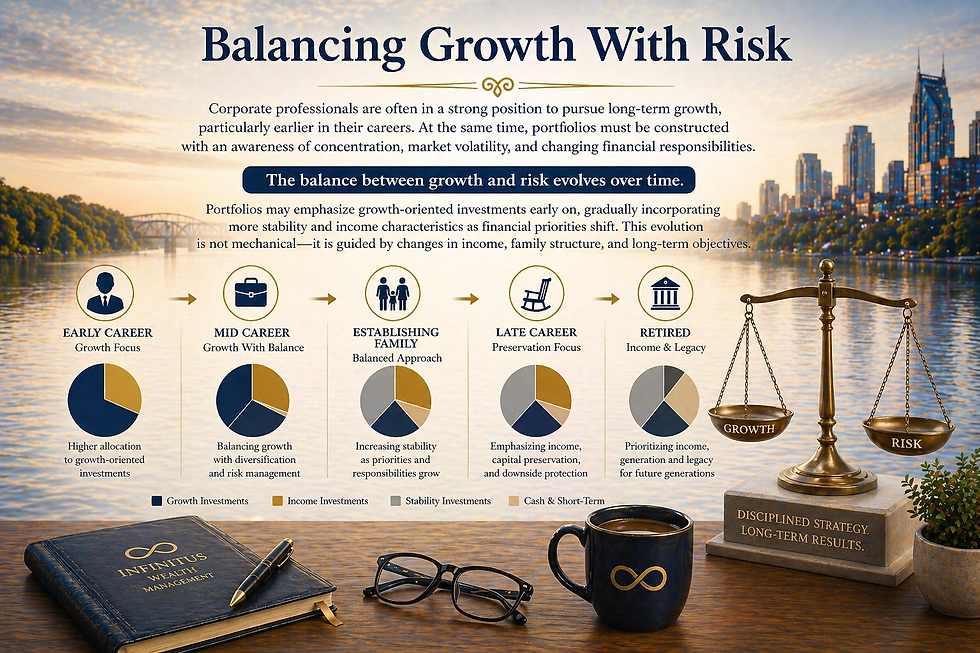

Retirement can last twenty-five to thirty-five years. In many cases, it remains a long-term investment horizon. That means retirees still need growth—but growth pursued with prudence.

The best advisors understand this balance.

What Retirees in Nashville Should Look for in a Financial Advisor

The Nashville advisory landscape is broad. National firms, banks, planners, brokers, and independent firms all compete for attention. Yet not all advisors serve retirees in the same way.

For households with meaningful assets, the search should center on capability, alignment, and service.

1. Active & Personalized Portfolio Management

Many retirees do not want a one-size-fits-all model portfolio placed on autopilot.

They prefer a strategy built around their specific needs:

Spending requirements

Risk tolerance

Family circumstances

Legacy goals

Tax profile

Time horizon

Existing holdings

A personalized portfolio should reflect the investor—not merely the software template.

2. Retirement Income Strategy

Generating retirement income is more nuanced than simply withdrawing funds annually.

An experienced advisor should understand how to coordinate:

Social Security timing

Required Minimum Distributions

Dividend and bond income

Cash reserve strategy

Tax brackets

Withdrawal sequencing

Market conditions

Poor withdrawal decisions can create avoidable tax costs or shorten portfolio longevity.

3. Risk Management & Capital Preservation

Retirees often care less about maximizing upside in euphoric markets and more about protecting capital when conditions deteriorate.

This can include:

Diversification discipline

Quality-focused holdings

Cash management

Fixed income structure

Tactical rebalancing

Sensible position sizing

Emotional discipline during volatility

A severe drawdown early in retirement can be especially damaging. Strong advisors respect that reality.

4. Tax-Aware Investing

For many affluent retirees, taxes become one of the largest annual expenses.

Thoughtful advisors may help improve after-tax outcomes through:

Strategic withdrawals

Capital gains management

Roth conversion analysis

Asset location decisions

Municipal bond strategies where appropriate

Tax-sensitive rebalancing

The goal is not complexity for complexity’s sake. It is preserving more of what has been earned.

5. Personal Relationship & Accessibility

Retirees often value knowing exactly who is managing their assets.

Many prefer direct communication with a principal advisor rather than rotating service teams or call centers.

Why Many Retirees Prefer Independent Wealth Management Firms

Large national institutions offer scale and recognizable brands. Yet scale is not always the same thing as personalization.

Many retirees increasingly prefer boutique independent firms because they often provide:

Direct access to the decision-maker

Customized portfolios

Greater accountability

More responsive service

Advice centered on the client rather than product quotas

Long-term relationship continuity

For investors who have spent decades building wealth, this model can feel more aligned.

Why Nashville Has Become a Retirement Wealth Hub

Nashville has evolved into one of the country’s most dynamic cities. Strong economic growth, cultural appeal, healthcare leadership, and Tennessee’s tax advantages have drawn affluent households from across the nation.

Many retirees relocating to Nashville arrive with more sophisticated financial needs than traditional planning alone can address.

They may hold:

Seven-figure taxable portfolios

Large IRAs or 401(k) rollovers

Concentrated stock positions

Real estate assets

Trust structures

Business sale proceeds

Family wealth transfer objectives

These circumstances often call for investment judgment as much as planning.

What Sophisticated Retirees Often Want Today

The modern retiree is not necessarily looking for a binder full of projections and little else.

Many seek:

Clear strategy

Ongoing portfolio oversight

Rational communication during turbulence

Modern technology and account access

Tax awareness

Transparent fees

Confidence that someone serious is paying attention

That combination can be difficult to find.

Why Infinitus Wealth Management May Appeal to Retirees

For retirees seeking a more investment-focused and personalized relationship, Infinitus Wealth Management offers a model that may resonate with discerning households.

Independent Boutique Structure

As an independent firm, Infinitus is positioned to prioritize client interests rather than large-firm product agendas or bureaucratic layers.

Active & Personalized Portfolio Management

Portfolios are approached through an active lens, emphasizing research, thoughtful allocations, risk awareness, and strategies tailored to the individual client.

Institutional Mindset, Personal Relationship

The firm combines sophisticated investment thinking with direct, high-touch service—an approach many retirees prefer over impersonal enterprise models.

Elite Investment Credibility

The firm’s leadership background includes education from The Wharton School, consistently ranked the world’s best business school. For clients, this signals rigorous financial training and a high standard of analytical discipline.

Leadership Under Pressure

A Purple Heart military background reflects resilience, steadiness, discipline, and composure under difficult conditions—qualities many investors value when markets become unsettled.

Tax-Aware Investing

Retirees often appreciate an advisor who understands that net returns—not just gross returns—matter.

Capital Preservation With Growth

The objective is not reckless risk-taking. It is prudent portfolio management designed to preserve purchasing power, seek growth, and manage downside exposure.

High-Touch Client Experience

Many retirees value prompt communication, personal attention, and knowing their advisor understands their family and priorities.

Superior Investment Returns—Framed the Right Way

Retirees understandably want strong investment results. Yet experienced investors know that chasing performance headlines can be dangerous.

The more prudent objective is to seek superior long-term risk-adjusted outcomes through:

Intelligent security selection

Tactical asset allocation

Cost awareness

Tax efficiency

Risk management

Patience and discipline

That philosophy tends to be more durable than speculation or trend chasing.

Questions Retirees Should Ask Before Hiring an Advisor

Before selecting any advisor in Nashville, retirees may wish to ask:

Who directly manages the portfolio?

Is the strategy customized or standardized?

How do you manage risk in retirement?

How do you approach taxes?

What happens during severe market declines?

How often are portfolios reviewed?

How are fees structured?

Will I work directly with the advisor?

How do you balance growth with preservation?

What distinguishes your firm from larger competitors?

The quality of the answers often matters more than the marketing.

Why the Right Advisor Relationship Matters

A strong advisor relationship can bring more than investment returns.

It can provide:

Organization

Perspective

Reduced financial stress

Better decision-making during volatility

Confidence in spending decisions

Continuity for spouses and family members

A trusted long-term sounding board

For many retirees, that peace of mind has real value.

Final Thoughts: Choosing the Best Financial Advisor for Retirees in Nashville

The best financial advisor for retirees in Nashville is ultimately the advisor whose philosophy, experience, discipline, and service model align with your needs.

For some, that may be a large institution. For many affluent retirees seeking customized portfolios, direct access, thoughtful tax strategy, and active oversight, an independent boutique firm can be a compelling alternative.

Retirement is not the end of wealth management. In many ways, it is when wealth management matters most.

For households seeking a more serious, personalized, and investment-focused approach, Infinitus Wealth Management represents a modern option rooted in discipline, stewardship, and long-term thinking.

Build a strategy that lasts beyond today.

The High-Net-Worth Wealth Management Checklist for Families With $5M to $25M

Managing Portfolio Risk When Your Income and Stock Are Tied to One Company

Generating Income with Stock Options: Strategies and Insights

Navigating Tax Implications for High Net Worth Individuals: Strategies to Reduce Your Taxes

Important Disclosures

Infinitus Wealth Management is a registered investment advisory firm. This article is provided for educational and informational purposes only and does not constitute investment, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any security or to enter into any advisory relationship. Any references to specific strategies, withdrawal rates, tax provisions, or historical figures are general in nature and may not be appropriate for any individual investor.

Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Tax laws are complex, change frequently, and have unique application to individual circumstances; please consult a qualified tax professional regarding your specific situation. Social Security rules, Medicare rules, and retirement account regulations are subject to legislative and regulatory change.

The information in this article was believed to be accurate at the time of writing but is not guaranteed. Readers should consult with their own qualified advisors before making any financial decisions specific to their situation.