How High-Net-Worth Family Investment Portfolios Are Structured Differently

- Erik James Roberts, Founder & Chief Investment Officer | Infinitus Wealth Management

- Jun 12

- 7 min read

There is a quiet myth in wealth management: that the path to a better high-net-worth family investment portfolio runs through ever more exotic products—private equity funds, hedge funds, layered alternative vehicles, and the family-office machinery that surrounds them. After more than a decade across this industry—first at Merrill Lynch, then at Edward Jones—I have come to a different conclusion. The families who do this best do not win because they bought their way into the most complicated structures. They win on cost, tax control, and ownership. They win because someone built them a real portfolio, holding by holding, around their actual situation.

That is the entire premise behind how we build a high-net-worth family investment portfolio at Infinitus Wealth Management. We do not assemble portfolios out of mutual funds, and we rarely reach for an ETF. We construct each client’s portfolio from individual stocks and individual bonds, chosen specifically for them, actively managed, and hedged where appropriate with options strategies. No models. No packaged products. No one-size-fits-most allocation pulled off a shelf. This article lays out why that structure is the genuinely sophisticated choice—and why the complexity that gets marketed to wealthy families so often works against them.

What a High-Net-Worth Family Investment Portfolio Is Really Competing Against

Most portfolios—even large ones—are quietly losing ground to their own structure before a single market move happens. The vehicles themselves impose a cost. A mutual fund charges an expense ratio every year whether it outperforms or not, and it can hand you a taxable capital-gain distribution in a year your account went down, because other investors in the same fund forced selling you never asked for. A model allocation or ETF sleeve is cheaper, but it still strips away the single most valuable thing a high-net-worth family investment portfolio can have: control at the level of the individual holding.

When you own a pooled fund, you own a slice of someone else’s decisions. You cannot harvest a loss on one specific position while holding the rest. You cannot gift a single appreciated lot to a family member or a donor-advised fund. You cannot place a protective put on the one concentrated stock that keeps you up at night. You inherit the fund’s embedded gains, its turnover, and its tax timing—and you pay for the privilege. The drag is real, it compounds, and it is almost entirely avoidable.

This is the comparison that matters, and it is the one the product industry would rather not foreground. A custom portfolio of individual securities removes the product expense ratio entirely, eliminates forced capital-gain distributions, and turns tax-loss harvesting from something you miss into something you control. None of that requires a hedge fund or a family office. It requires direct ownership and an advisor whose only job is building your portfolio.

How We Build a High-Net-Worth Family Investment Portfolio at Infinitus

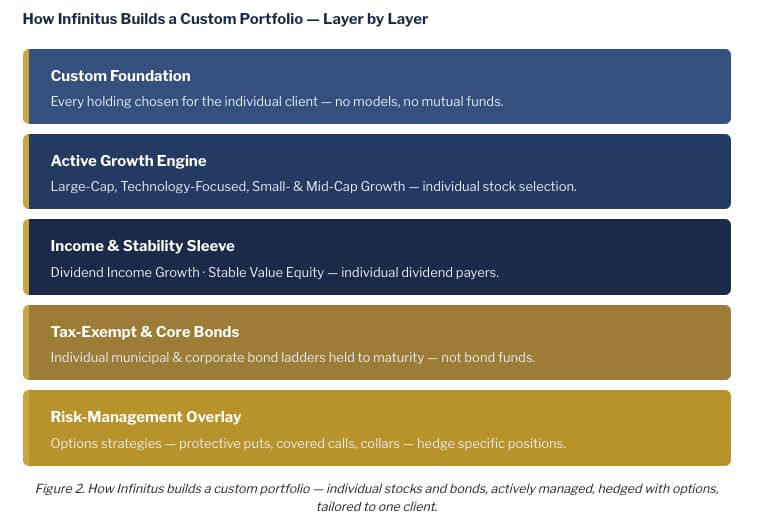

A high-net-worth family investment portfolio at Infinitus is built in functional layers, and every layer is constructed from individual securities we select and manage directly. The diagram below shows how the pieces fit together—and notice what is absent: there is no fund layer, no model sleeve, no outside manager taking a second fee. Each layer is assembled from our own strategies, tailored into one custom portfolio.

The active growth engine

The core of most portfolios is equity, and we build it from individual companies—not an index wrapper. Depending on the client, that engine draws on our Large-Cap Growth, Technology-Focused Growth, and Small- & Mid-Cap Growth strategies, with each position selected on its own merits. Direct ownership is what makes the rest of the structure possible: it is the reason we can harvest losses surgically, gift specific lots, and hedge individual names. A high-net-worth family investment portfolio built on individual stock selection is simply more deliberate, and the tax control it unlocks is worth real money over time.

The income and stability sleeve

For clients who need yield, ballast, or both, we build an income sleeve from individual dividend-paying companies through our Dividend Income Growth and Stable Value Equity strategies, and we blend in Balanced Growth Equity where a steadier ride is the priority. Because these are individual holdings rather than a fund, the client keeps control of the cost basis and the timing of every gain—and the dividends arrive without a fund manager’s overlay skimming the return.

The fixed income ladders

We build bond exposure the same way the most disciplined investors always have: as ladders of individual bonds held to maturity, not as bond funds whose share price swings with rates regardless of what the underlying bonds are doing. Through our Tax-Exempt Municipal Bonds and U.S. & Global Bonds strategies, we tailor duration, credit quality, and cash-flow timing to the client. For families in high tax brackets, an individual municipal ladder can deliver a tax-equivalent yield that beats taxable alternatives of similar quality—a genuine return advantage, not just a shelter.

The risk-management overlay

This is where direct ownership pays off most visibly. Because we hold individual securities, we can hedge specific positions with advanced options strategies—protective puts to limit downside on a concentrated holding, covered calls to generate income against existing positions, and collars to define a range of outcomes around a stock a client does not want to sell for tax or personal reasons. Our Risk-Controlled Growth strategy is built around exactly this discipline. A pooled fund cannot do any of it; you cannot put a collar on a mutual fund share. Hedging at the position level is only possible when you own the positions.

A high-net-worth family investment portfolio should be built around the client, not assembled from products built for the average investor. We construct each portfolio from individual stocks and bonds, actively manage it, and hedge it with options—fee-only, with no commissions and no proprietary products. The structure itself is the edge.

What About Private Markets and Alternatives?

It is fair to ask where private equity, hedge funds, and other alternatives fit. The honest answer is that for most families they are oversold. The marketing emphasizes a historical return premium; it tends to omit the layered fees, the multi-year lockups, the opacity about what you actually own, and the brutal dispersion between top and bottom managers—the gap that means the average investor in alternatives often earns far less than the headline figures suggest. Illiquidity is not a virtue in itself, and complexity is not the same as sophistication.

Where genuine private-market exposure makes sense for a client, we handle it directly through our Private Companies strategy rather than outsourcing it to an opaque fund with a second layer of fees. That keeps the same principles intact that govern the rest of the portfolio: direct ownership, transparency, and alignment. The point is not that private assets are never appropriate—it is that they should clear a high bar, on our terms, inside a portfolio we built, rather than being treated as the aspirational endpoint every wealthy family is supposed to chase.

The Strategies Behind a Custom Infinitus Portfolio

Our twelve proprietary strategies are not products a client buys into. They are the building blocks we draw on to construct one custom portfolio for each client. The table below maps the role each part of a high-net-worth family investment portfolio plays to the Infinitus strategies that build it.

Two clients with similar net worth can end up with very different portfolios, because the strategies are combined and weighted around each client’s tax situation, income needs, concentration risk, and goals. That is what “custom” actually means—not a risk-tolerance questionnaire mapped to a model, but a portfolio assembled holding by holding.

Why This Wins for a High-Net-Worth Family Investment Portfolio

Strip away the marketing and the advantages of this approach are concrete:

Cost control: no fund expense ratios skimming returns every year, and no second layer of fees from outside managers.

Tax control: losses harvested surgically, appreciated lots gifted directly, and gains realized on the client’s timing, not a fund’s.

Risk control: options hedging applied to specific holdings, which is only possible because the client owns those holdings directly.

True customization: individual securities selected and weighted for one person’s situation, not a model designed for the median investor.

Independence: fee-only and fiduciary, with no commissions, no proprietary products, and no revenue-sharing arrangements pulling against the client.

You do not need a twenty-five-million-dollar family office to get this. You need an advisor who builds you a genuine portfolio of individual companies and bonds and actively manages the risk inside it. That is the standard a serious high-net-worth family investment portfolio should be held to—and it is exactly what we do.

Talk to Infinitus About Building Your Custom Portfolio

At Infinitus Wealth Management, we build every client a custom portfolio from individual stocks and individual bonds—never mutual funds, rarely an ETF—actively managed and hedged with options where it strengthens the portfolio. We are an independent, fee-only fiduciary: no commissions, no proprietary products, no conflicts pulling against you. Our twelve proprietary strategies give us the range to tailor a portfolio to your tax situation, income needs, and goals, whether you are early in building serious wealth or managing well into eight figures.

If you would like a clear-eyed look at how your current portfolio is actually structured—what it is costing you in fees and tax drag, whether it is being managed at the level of individual holdings, and whether your advisor’s incentives are genuinely aligned with yours—we welcome the conversation. Our complimentary portfolio analysis gives you an objective, holding-level assessment and a direct view of what a custom Infinitus portfolio would look like for you.

The High-Net-Worth Wealth Management Checklist for Families With $5M to $25M

Managing Portfolio Risk When Your Income and Stock Are Tied to One Company

Generating Income with Stock Options: Strategies and Insights

Navigating Tax Implications for High Net Worth Individuals: Strategies to Reduce Your Taxes

Important Disclosures

Infinitus Wealth Management is a registered investment advisory firm. This article is provided for educational and informational purposes only and does not constitute investment, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any security or to enter into any advisory relationship. Any references to specific strategies, withdrawal rates, tax provisions, or historical figures are general in nature and may not be appropriate for any individual investor.

Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Tax laws are complex, change frequently, and have unique application to individual circumstances; please consult a qualified tax professional regarding your specific situation. Social Security rules, Medicare rules, and retirement account regulations are subject to legislative and regulatory change.

The information in this article was believed to be accurate at the time of writing but is not guaranteed. Readers should consult with their own qualified advisors before making any financial decisions specific to their situation.