What to Do With a Music Advance or Music Catalog Sale

- Erik James Roberts, Founder & Chief Investment Officer | Infinitus Wealth Management

- 1 day ago

- 11 min read

A framework for deploying a large, one-time music payday without losing it to taxes or lifestyle.

A music catalog sale is one of the largest financial events a songwriter or artist will ever experience — a single wire that can equal a decade of touring, recording, and royalties arriving all at once. The same is true, on a smaller scale, of a publishing or label advance. These are extraordinary opportunities. They are also fragile ones. The money tends to arrive without an owner’s manual, and the two forces most likely to erode it — taxes and lifestyle creep — go to work immediately, quietly, and often irreversibly.

The artists who keep their windfalls are rarely the ones who earned the most. They are the ones who treated a music catalog sale or advance as a one-time capital event rather than a raise, sequenced their decisions in the right order, and rebuilt a durable income stream out of the lump sum. This is a framework for doing exactly that. It is written for a moment in the market — 2025 and 2026 — in which catalog buyers have re-entered with real capital, and the decisions you make in the ninety days after the check clears will shape the next thirty years.

The goal isn’t to spend the payday well. It’s to convert a stream you sold into a portfolio you own — and to keep the IRS from taking more than the law requires.

The Two Paydays Are Not the Same

Before you deploy a dollar, understand which kind of money you’re holding, because the tax code treats an advance and a music catalog sale completely differently — and that difference is worth more than almost any investment decision you’ll make afterward.

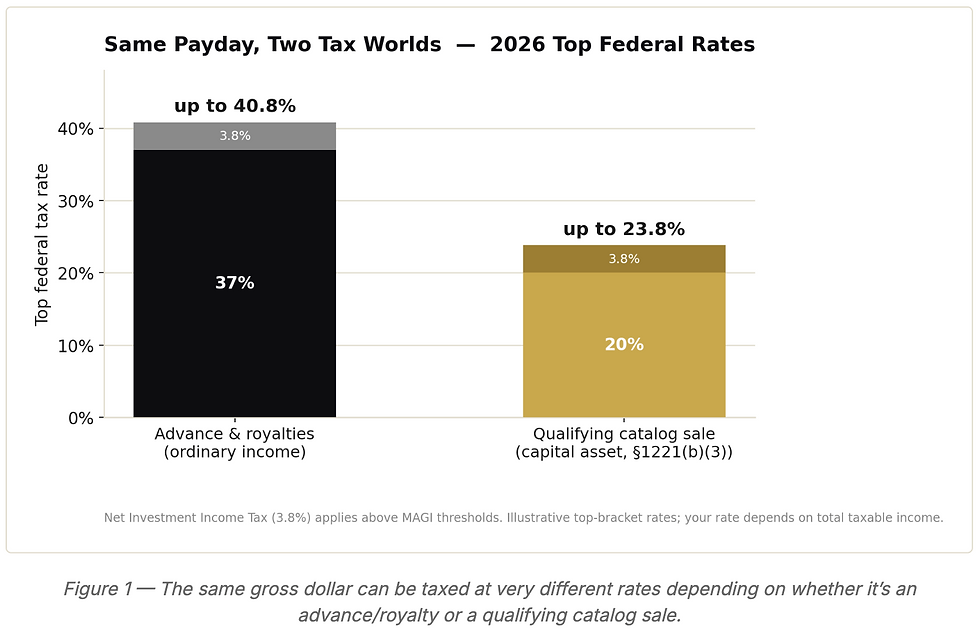

An advance is ordinary income. Whether it comes from a label or a publisher, an advance is generally recoupable — the company recovers it out of your future royalties before you see another dollar — and it is taxed as ordinary income in the year you receive it, at rates reaching 37% federally for top earners. Royalties themselves are taxed the same way. An advance is not “free” money; it is your own future earnings, pulled forward, taxed at the highest rates in the code, and owed back to the company before your account turns positive again.

A catalog sale can be a capital asset. Here the code does something unusual and generous. Under Section 1221(b)(3) — the result of the Songwriters Capital Gains Tax Equity Act of 2006, driven largely by the Nashville Songwriters Association International — a songwriter may elect to treat the sale of self-created musical compositions as the sale of a capital asset. Held longer than a year, that gain is taxed at long-term capital-gains rates topping out at 20%, not 37%. Painters, authors, and most other creators don’t get this. Songwriters do. It is one of the few provisions in the tax code written specifically in favor of the people who make the music.

One nuance worth stating plainly, because honesty matters more than a clean headline: the capital-gains election is clearest for musical compositions (the songwriting / publishing side). The treatment of master recordings — the actual sound recordings — is less settled, and the structure of a combined deal can affect how different pieces are taxed. This is precisely the kind of detail where a few hours with a qualified tax attorney before signing can be worth six figures after.

Why the Tax Bill Is the First Problem to Solve

The single most expensive mistake after a music catalog sale is spending or investing the gross number. The money in your account is not yours yet — a meaningful slice belongs to the government, and it comes due whether or not you set it aside. Solve that first, in writing, before anything else.

For 2026, long-term capital gains are taxed at 0%, 15%, or 20% depending on taxable income. The top 20% rate applies once taxable income exceeds roughly $545,500 for single filers and $613,700 for married couples filing jointly — thresholds a large catalog sale will clear in a single stroke. On top of that, high earners owe the 3.8% Net Investment Income Tax, pushing the effective federal ceiling to about 23.8%. That is still dramatically better than the 40.8% an equivalent advance could face, but on a seven-figure deal it is real money, and it is due at tax time.

Three levers can change the outcome — and all of them must be pulled before you sign, not after:

Where you live when you sell. Capital-gains tax is layered: federal plus state. A songwriter selling from California can face state tax as high as 13.3% on the same gain that a Nashville resident pays nothing on — Tennessee has no state income tax. For an artist genuinely relocating, establishing legal domicile in a no-income-tax state well before a sale can be one of the largest “returns” available, but residency rules are strict and fact-specific; this is a planning decision, not a paperwork trick.

How you receive the money. An installment sale spreads the proceeds — and the gain — across several tax years, which can keep more of it in lower brackets and smooth the bill. It also introduces buyer-credit risk, so the structure has to be weighed, not assumed.

When you sell relative to your other income. A year in which touring income is low may be a more efficient year to recognize a large gain than a peak earnings year.

None of this is a substitute for a CPA and a tax attorney who specialize in music. It is the opposite — it’s the reason to engage them before the deal closes, while the structure is still movable. Once the wire hits, most of these levers are gone.

The Lifestyle Trap: Why a Big Check Disappears

Taxes are the visible threat. Lifestyle creep is the quiet one, and it has ended more careers’ worth of wealth than any market crash. The psychology is understandable: a music catalog sale feels like validation, like permanence, like the end of financial worry. So the spending decisions that follow get made as if the income that produced the catalog is still coming in — when, by definition, you just sold the future income that was coming in.

Music income is lumpy. A catalog or an advance is not a salary; it is a one-time conversion of years of work into a single number. The house, the cars, the generosity to family, the “small” recurring commitments — each one is funded out of principal, and principal that’s been spent can’t generate income. The artists who struggle five years after a windfall almost never blame a single extravagance. They describe a hundred reasonable-seeming decisions, each made against a balance that felt infinite and wasn’t.

Treat the payday as the last paycheck from an old job — not the first of a new, larger one.

The discipline that protects you is unglamorous: decide on the tax reserve and the long-term portfolio first, automate them, and let yourself enjoy what’s genuinely left over — a defined amount, not an open tab against the whole balance.

A Framework for Deploying the Proceeds

Sequence matters more than selection. The order in which you assign the money is what determines whether a music catalog sale becomes lasting wealth or a memorable year. Work through these four buckets in order, and only move to the next once the prior one is fully funded.

1. Fund the tax reserve first. Before you celebrate, move the estimated tax — confirmed with your CPA — into a separate, safe, liquid account, and don’t touch it. Treasury bills or a high-grade money-market position can hold it and earn something while it waits. This money was never yours to deploy.

2. Build a cash buffer. Because music income is irregular, a meaningful cash reserve — often twelve to twenty-four months of actual living expenses — is not idle money; it’s what keeps you from being forced to sell investments at a bad time or take the next deal on someone else’s terms. It is the foundation that lets the rest of the portfolio stay invested through volatility.

3. Clear high-cost debt. Paying off high-interest debt is a guaranteed, tax-free return equal to the interest rate you were paying — a return most investments can’t promise. Low-rate, tax-advantaged debt (a reasonable mortgage) is a more nuanced decision and doesn’t automatically belong here.

4. Put the remainder to work in an income-producing portfolio. This is the bucket that replaces what you sold. Everything above is defense; this is where a catalog sale is converted back into a stream you control. We’ll spend the rest of this article here, because it’s where the long-term outcome is decided.

Turning a Music Catalog Sale Into a Durable Income Stream

Here is the insight most windfall advice misses: when you complete a music catalog sale, you didn’t just receive money — you gave something up. You traded a future stream of royalties for a lump sum today. And catalog royalties, left alone, tend to decay: streams fade, sync placements end, the long tail thins out. The buyer paid you a price that reflects that decline. The financial task, then, isn’t to “invest some of the windfall.” It’s to rebuild an income stream — ideally a more stable and growing one — out of the principal you now hold.

At Infinitus, that rebuilding is done with individual stocks and bonds, not packaged products. The reasons are specific to a situation like this:

A bond ladder for predictable income. A ladder of individual high-grade and municipal bonds can produce scheduled, predictable cash flow with defined maturity dates — income you can actually plan a life around. For a Tennessee-based artist with no state income tax, tax-exempt municipal bonds can be especially efficient, delivering federally tax-advantaged income without adding a state-tax layer.

Dividend-growth equities to outpace inflation. Owning shares of established, cash-generative companies with a history of raising their distributions creates an income stream designed to grow over time — the antidote to the decaying royalty curve you sold. You hold the actual companies, not a fund wrapper, which means transparency on exactly what you own and control over the tax consequences of every position.

Options-based hedging on concentrated or large positions. When a single large position needs protecting — or when you simply want to manage downside on a meaningful holding — strategies such as protective puts (which set a floor under a position), covered calls (which generate income against shares you hold), and collars (which combine the two to define a range) can be used deliberately to manage risk and produce cash flow. These are tools, used position by position, not blanket bets.

The throughline is ownership and control. A music catalog sale hands you, often for the first time, full command over your own balance sheet. Building that balance sheet from individual securities — rather than handing it to opaque, illiquid vehicles — keeps you liquid, keeps the tax treatment in your hands, and keeps the income visible and adjustable as your life changes.

A Word on Timing: The 2026 Catalog Market

Context helps you negotiate. After a cooling in 2023–2024 as interest rates rose, the catalog market re-opened with real capital in 2025 and into 2026. Industry valuation specialists priced hundreds of catalogs worth roughly $13 billion combined in 2025, and headline activity returned — a reported $200 million catalog transaction for Britney Spears with Primary Wave, and a joint vehicle of up to $1.2 billion earmarked by Warner and Bain Capital for acquisitions. Multiples that had peaked above 18x net publisher’s share in 2021 settled into a roughly 12x–18x range, with publishing and well-aged catalogs commanding the top end and younger material trading lower.

Two practical implications for anyone weighing a music catalog sale right now. First, clean rights documentation drives the multiple — resolved co-writer splits, registered works, cleared samples. Unclear rights can discount an offer by a wide margin or kill a deal outright; tightening your paperwork before going to market is among the highest-return work you can do. Second, buyers are increasingly pricing in optionality like AI-training licensing as upside — a reason not to assume the first offer reflects the full value, and to have experienced representation at the table.

Five Mistakes That Quietly Destroy a Windfall

Spending against the gross. Living off the pre-tax number guarantees a painful reconciliation at tax time. Reserve first.

Chasing illiquid alternatives. A windfall attracts pitches — private deals, funds with long lockups, “can’t-miss” ventures. Illiquidity is a real cost, and complexity often hides risk and fees. Skepticism here is a feature, not timidity.

Becoming the family bank. Generosity is a value worth honoring — but undocumented, open-ended lending against principal is one of the most common ways large sums quietly disappear. Decide on a defined gifting amount inside your plan, not in response to each request.

Leaving the proceeds in cash for years. Fear of a mistake leads many artists to park a catalog sale in cash indefinitely. Inflation makes that its own slow loss. A deliberate, staged deployment is the middle path.

No written plan and no fiduciary. A windfall managed by instinct, or by an advisor paid on commission for what they sell you, rarely ends where it should. The structure you put around the money matters as much as the money.

How Infinitus Approaches a Music Payday

Infinitus Wealth Management is a Nashville-based, fee-only fiduciary registered investment adviser — which means we are paid by our clients, never by commissions or product sponsors, and we are legally obligated to act in your interest. For musicians, songwriters, and entertainers navigating an advance or a music catalog sale, our work is investment-first: we build custom portfolios out of individual stocks and bonds, use options-based hedging where it serves a clear purpose, and coordinate closely with your CPA and tax attorney so the structure of the deal and the deployment of the proceeds are working together rather than against each other.

If you’re weighing an advance or a music catalog sale, the most valuable conversations happen before you sign. We offer a complimentary, no-obligation review of your situation — including a financial plan — to help you understand your options.

Talk to Infinitus About Building Your Custom Portfolio

At Infinitus Wealth Management, we build every client a custom portfolio from individual stocks and individual bonds—never mutual funds, rarely an ETF—actively managed and hedged with options where it strengthens the portfolio. We are an independent, fee-only fiduciary: no commissions, no proprietary products, no conflicts pulling against you. Our twelve proprietary strategies give us the range to tailor a portfolio to your tax situation, income needs, and goals, whether you are early in building serious wealth or managing well into eight figures.

If you would like a clear-eyed look at how your current portfolio is actually structured—what it is costing you in fees and tax drag, whether it is being managed at the level of individual holdings, and whether your advisor’s incentives are genuinely aligned with yours—we welcome the conversation. Our complimentary portfolio analysis gives you an objective, holding-level assessment and a direct view of what a custom Infinitus portfolio would look like for you.

The High-Net-Worth Wealth Management Checklist for Families With $5M to $25M

Managing Portfolio Risk When Your Income and Stock Are Tied to One Company

Generating Income with Stock Options: Strategies and Insights

Navigating Tax Implications for High Net Worth Individuals: Strategies to Reduce Your Taxes

Important Disclosures

Infinitus Wealth Management is a registered investment advisory firm. This article is provided for educational and informational purposes only and does not constitute investment, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any security or to enter into any advisory relationship. Any references to specific strategies, withdrawal rates, tax provisions, or historical figures are general in nature and may not be appropriate for any individual investor.

Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Tax laws are complex, change frequently, and have unique application to individual circumstances; please consult a qualified tax professional regarding your specific situation. Social Security rules, Medicare rules, and retirement account regulations are subject to legislative and regulatory change.

The information in this article was believed to be accurate at the time of writing but is not guaranteed. Readers should consult with their own qualified advisors before making any financial decisions specific to their situation.